A Guide to Infrastructure Project Structuring

Project structuring plays a central role in delivering infrastructure, including the UK’s ambitious infrastructure investment programme. The government’s infrastructure pipeline includes more than 660 projects, representing approximately £700–775 billion of planned investment over the next decade (National Infrastructure and Construction Pipeline, 2024).

However, infrastructure projects are not only capital-intensive; they are also characterised by long operating lives and exposure to a wide range of construction, operational and regulatory risks.

Because investors and lenders commit capital over extended periods, the successful delivery of a project depends on how these risks, responsibilities and revenue streams are allocated among the parties involved. The structure adopted for a project therefore has a direct influence on its bankability, financing arrangements and long-term sustainability. Against this backdrop, this article reviews the principal infrastructure project structures and the financing arrangements that support them.

Project Finance as the Foundation

Origins of Project Finance

Despite its widespread use today, project finance is not a recent development; its core logic is several centuries old. The earliest recorded instance dates to 1299, when the English Crown engaged a Florentine merchant bank to develop the Devon silver mines. The bank financed all operating costs in exchange for one year of the mines’ output, with no recourse to the Crown if the ore extracted proved insufficient (Esty & Christov, 2002).

The same principle resurfaced in the 1930s, when “wildcat” oil explorers in Texas and Oklahoma used production payment loans to fund oilfield exploration, with creditors looking solely to the project’s own cash flows rather than to the borrower (Esty & Christov, 2002).

This reliance on project-generated revenues rather than sponsor guarantees remains the defining feature of project finance today. Its modern form emerged from the 1970s onwards, first through large natural resource developments such as BP’s Forties Field in the North Sea and later through the US power sector under the Public Utility Regulatory Policy Act of 1978.

By requiring utilities to purchase the full output of qualified producers under long-term contracts, the legislation provided the revenue certainty needed to support non-recourse debt financing. The contractual framework that emerged from these projects continues to underpin infrastructure financing today (Esty & Christov, 2002).

SPV

At the centre of project finance structuring is the Special Purpose Vehicle (SPV). Project finance involves raising debt and equity for a discrete asset through an SPV, a company established solely to develop, own and operate the project. Because the SPV is legally separate from its sponsors, lenders rely primarily on the project’s assets, contracts and cash flows for repayment rather than on the sponsors’ balance sheets (Gorton & Souleles, 2005).

As a result, project finance is inherently contract-driven. Construction contracts, operating agreements, offtake arrangements, concession agreements and government support mechanisms are all designed to secure and protect the project’s future cash flows. Together, these agreements allocate risks among the various parties and provide the revenue visibility required by lenders. Consequently, the quality of a project’s contractual framework is a key determinant of its ability to raise debt financing (Gorton & Souleles, 2005).

Infrastructure projects are particularly well suited to this financing approach. Although they require substantial upfront capital expenditure, they typically generate stable and predictable revenues over long operating lives. These characteristics make it possible to structure financing around future project cash flows rather than sponsor creditworthiness. As discussed in our article on securing finance for renewable energy projects, developers must therefore carefully design both the project’s contractual structure and its financing mix in order to attract investors and achieve financial close.

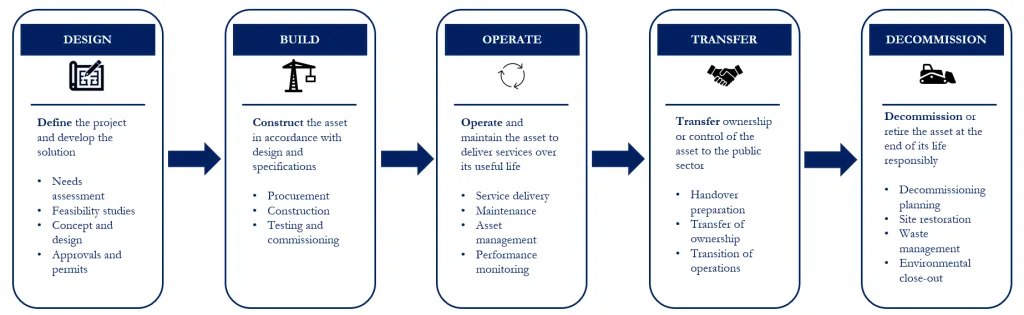

Infrastructure Project Lifecycle

Every infrastructure project follows a common lifecycle. Before examining the various contractual structures used to deliver infrastructure assets, it is useful to first consider the five core phases that underpin any project: Design, Build, Operate, Transfer, and Decommission. These phases serve as the fundamental building blocks of infrastructure delivery.

The key distinction between project structures lies in how responsibility for each phase is allocated between public and private sector participants.

Design

The Design phase covers the technical, environmental and financial preparation of a project before construction begins. Key activities include feasibility studies, FEED studies, environmental assessments, permitting and, where relevant, grid connection arrangements. It also produces the documentation required for financing, including the financial model and project agreements used by lenders during due diligence. The party responsible for design bears the risk of inaccurate cost estimates, permitting delays and design deficiencies.

Build

The Build phase runs from financial close to the commercial operations date (COD), when the asset becomes operational and begins generating revenue. Construction is typically financed through sponsor equity and senior debt, with funds released as construction milestones are achieved. Delivery is usually governed by an EPC contract, under which the contractor agrees to complete the project on a fixed-price, date-certain basis and meet specified performance standards. This structure helps protect the project against cost overruns, delays and underperformance.

Operate

The Operate phase begins once the asset reaches commercial operations and continues throughout its operating life, often for 20 to 40 years. During this period, the operator is responsible for maintaining the asset and meeting the performance standards required under the relevant contractual framework. Revenues are typically generated through mechanisms such as Power Purchase Agreements (PPAs), availability payments under PPPs, or regulated tariffs under a RAB model. The stability and predictability of these cash flows are critical to supporting debt repayment and generating returns for investors.

Decommission

The Decommission phase takes place at the end of the asset’s life and includes dismantling, site restoration and environmental remediation. Responsibility for these activities depends on the project structure and ownership arrangements. In some cases, decommissioning costs are funded through reserves accumulated during the operating phase, while in others responsibility transfers to the public sector upon handover of the asset.

Infrastructure Project Lifecycle

Project Structuring

In project finance structuring, the project structure is a contractual decision about which phases the private sector takes on and which the public sector retains. Each combination produces a different risk profile, a different financing logic, and a different set of obligations for each party. The acronym names the phases the private party assumes, in the order they occur.

Design-Build (DB)

Design and construction are bundled into a single contract awarded to one counterparty, which assumes responsibility for both engineering and delivery. The defining logic is the elimination of interface risk, since a single party now bears the consequence of a design that proves expensive or difficult to build. Responsibility still ends at COD, with financing and operations remaining public.

Design-Build-Operate (DBO)

The private party takes on design, construction, and operation, running the asset for a defined period after COD while the public sector retains financing and ownership. The defining logic is the whole-life incentive created by linking construction and operation, since the contractor bears the operational consequences of its own design and build decisions and is discouraged from cutting corners during delivery. The public sector continues to carry capital and revenue risk throughout.

Design-Build-Finance (DBF)

The private party designs, builds, and finances the asset, deferring the public sector’s capital outlay until COD or spreading it across a repayment period. The core logic is balance sheet relief for the public sector, which converts an upfront capital requirement into a future payment obligation. Operational responsibility reverts to the public sector at handover, so the private party bears construction and financing risk but not operating risk.

Design-Build-Finance-Operate (DBFO)

The private party assumes design, construction, financing, and operation across the full active life of the asset up to transfer or concession expiry. Revenue is generally secured through an availability payment, under which the public authority pays a periodic fee conditional on performance rather than exposing the private party to demand risk. This is among the most common PPP structures, particularly in social and transport infrastructure.

The M25 motorway in England provides a representative example of project finance structuring under a DBFO model. Under a 30-year contract, the Connect Plus consortium assumed responsibility for the design, construction, financing and operation of the motorway. Remuneration is provided by the public authority rather than through direct user charges, with demand risk largely retained by the State while construction, financing and operating risks are transferred to the private sector. This allocation of responsibilities reflects the defining characteristic of the DBFO structure (Highways Agency, 2009).

Design-Build-Operate-Maintain (DBOM)

Under a DBOM structure, the private sector is responsible for designing, constructing, operating and maintaining the asset, while the public sector provides the financing.

Combining these responsibilities encourages the private party to consider the asset’s performance and maintenance requirements throughout its life rather than focusing solely on construction costs. Construction, operating and maintenance risks are transferred to the private sector, while the public sector retains financing responsibility.

Design-Build-Finance-Operate-Maintain (DBFOM)

The private party assumes design, construction, financing, operation, and maintenance, with maintenance set out as an explicit and separately enforced obligation throughout the operating period. The defining logic is maximum whole-life alignment, since the private party is bound to defined condition standards and suffers deductions from its availability payment for any shortfall. It represents the most comprehensive transfer of lifecycle responsibility to the private sector short of permanent ownership.

The proposed solar project at Botswana’s Karowe diamond mine provides a recent example of the DBFOM model. Under the tender, the selected developer will finance, construct, operate and maintain a solar facility of up to 30 MW under a long-term power purchase agreement. The project therefore transfers full lifecycle responsibility to the private sector in exchange for long-term contracted revenues (PV Magazine, 2026).

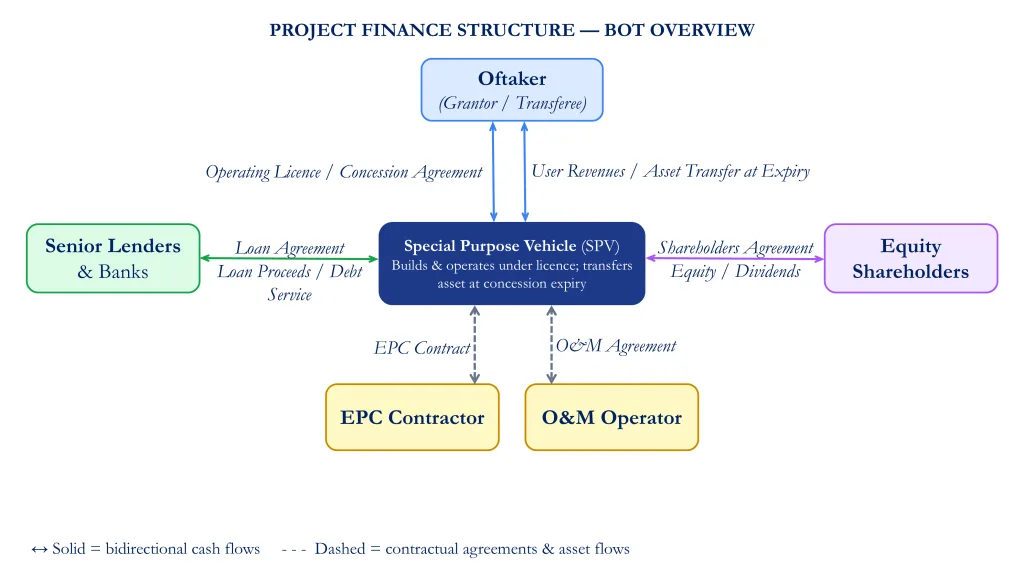

Build-Operate-Transfer (BOT)

The private party finances and constructs the asset, operates it across a defined concession period, and transfers it to the public sector at expiry at no or nominal cost. The defining logic is full investment recovery during the operate phase, with the private party earning its return through revenues before relinquishing the asset.

Design is typically led or shared by the public sector, and ownership during the concession rests on an operating licence rather than legal title.

Build-Own-Operate-Transfer (BOOT)

The private party constructs the asset, holds legal title to it throughout the concession, operates it, and conveys title to the public sector at expiry. The defining logic is the strengthened lender security that ownership provides, since the SPV can grant a charge over the asset itself in addition to its contractual rights. This makes the structure common where lender security requirements are stringent, such as in power generation.

The Channel Tunnel provides a representative example of project finance structuring under a BOOT model. Eurotunnel designed, built, owned and operated the asset under a long-term concession, after which ownership reverts to the British and French governments (Global Infrastructure Hub, 2020). The project combined private financing with temporary private ownership, reflecting the defining characteristic of the BOOT model: private ownership and operation during the concession period followed by transfer to the public sector.

Build-Transfer-Own-Operate (BTOO)

The private party builds the asset and transfers legal title to the public sector immediately on completion, then retains economic ownership and operating rights for the concession period. The defining logic is the separation of legal title from economic ownership, satisfying a legal requirement for public ownership of strategic assets while preserving the private party’s rights to the project cash flows. Title therefore passes at the start of operations rather than the end.

Build-Finance-Operate (BFO)

The private party builds, finances, and operates the asset without ever taking ownership, which remains with the public sector throughout. The defining feature is the absence of both a design responsibility, typically retained or specified by the public sector, and a transfer phase, since title was never private to begin with. The private party recovers its capital through operating revenues or an availability stream across the operating period.

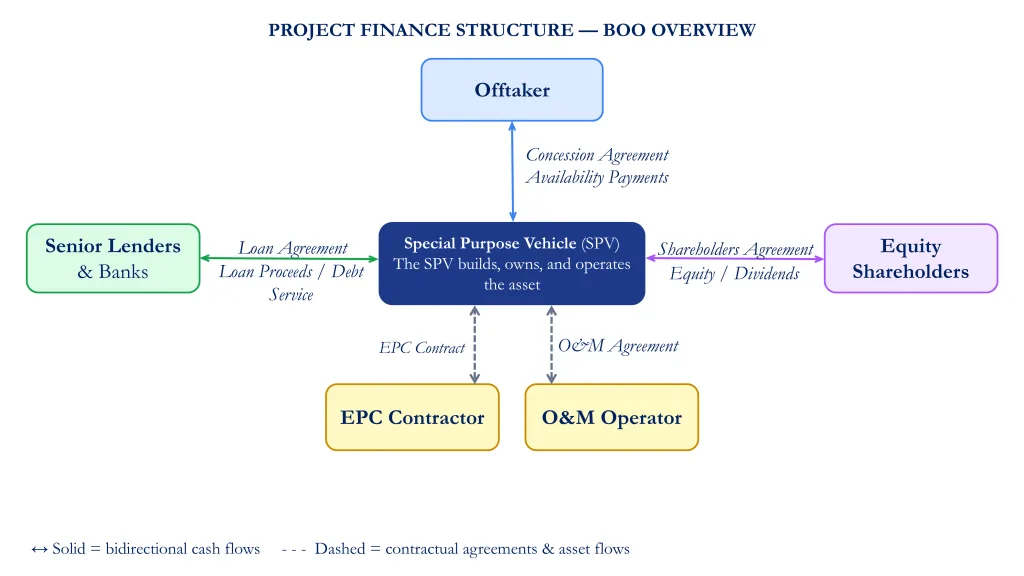

Build-Own-Operate (BOO)

The private party builds, owns, and operates the asset permanently, with no transfer phase and no reversion to the public sector. The defining logic applies where there is no policy rationale for eventual public ownership, leaving economic regulation rather than a concession endpoint as the primary discipline on the operator. Permanent ownership exposes the private party to long-term regulatory and residual value risk that transfer structures avoid.

South Australia’s Firm Energy Reliability Mechanism (FERM) provides a recent example of the BOO model. Under the scheme, private developers were awarded 15-year contracts to develop, own and operate six large-scale battery storage projects with a combined capacity of 1,334 MW. The assets remain under private ownership throughout their operating life, reflecting the core characteristic of the BOO structure: permanent private ownership and operation of the asset (Energy-Storage.News, 2024).

Build-Lease-Transfer (BLT)

The private party builds the asset and leases it to the public sector for a defined period, during which the public sector operates it and makes lease payments, before ownership transfers at the end of the term. The defining logic isolates the private party’s return in a lease payment stream, so it bears construction and financing risk but not operational or demand risk. The arrangement functions economically like an instalment purchase by the public sector.

Build-Finance-Lease-Transfer (BFLT)

The private party builds and finances the asset, leases it to the public sector over the concession period, and transfers ownership at the end of the term. The defining logic resembles a long-dated secured loan from the private party to the public sector, with the asset serving as collateral and the lease payments functioning as principal and interest. It is used where governments seek to defer capital expenditure without formally recognising debt.

Structure Comparison

| Structure | Title during concession | Transfer at end | Who bears demand risk | Typical sector | Revenue mechanism |

| DB (Design-Build) | No, public authority retains title | Not applicable | Public | Public buildings, roads, schools | Public budget payments |

| DBO (Design-Build-Operate) | No, public authority retains title | Not applicable | Usually public | Water treatment, transport infrastructure | Availability payments or service fees |

| DBF (Design-Build-Finance) | Usually no, ownership transferred upon completion | Yes, to public authority at completion | Public | Public infrastructure, social infrastructure | Public repayment of finance works |

| DBFO (Design-Build-Finance-Operate) | Typically no, operates under concession | Yes, to public authority | Usually public through availability mechanism | Roads, highways, transport infrastructure | Availability payments or shadow tolls |

| DBOM (Design-Build-Operate-Maintain) | No, public authority retains title | Not applicable | Public | Water, wastewater, public facilities | Service payments or availability payments |

| DBFOM (Design-Build-Finance-Operate-Maintain) | Usually concession-based, title often public | Yes, to public authority | Private or shared, depending on contract | PPP transport, social infrastructure, utilities | User charges, availability payments, or hybrid |

| BOT (Build-Operate-Transfer) | No, operates under licence | Yes, to the state | Private, user pays, shifting to public | Transport such as roads, airports, ports | User charges or availability payments |

| BOOT (Build-Own-Operate-Transfer) | Yes, developer holds title | Yes, title reverts | Private or public, depending on mechanism | Power generation, utilities | Offtake payments or availability payments |

| BTOO (Build-Transfer-Own-Operate) | Asset transferred initially, then private operating rights granted | Usually no further transfer | Public or shared | Utilities, industrial infrastructure | User fees or contractual payments |

| BFO (Build-Finance-Operate) | Usually no permanent ownership | Depends on contract | Private or shared | Transport, utilities | User charges or availability payments |

| BOO (Build-Own-Operate) | Yes, permanent ownership | No transfer | Private, under regulation | Liberalised markets, renewables | Regulated tariff or market sales |

| BLT (Build-Lease-Transfer) | Usually private during lease term | Yes, to public authority | Public | Schools, hospitals, public buildings | Lease payments from public authority |

| BFLT (Build-Finance-Lease-Transfer) | Usually private during lease term | Yes, to public authority | Public | Social infrastructure, government facilities | Lease payments covering financing and operation |

Financing Structures and Revenue Models

The structures discussed above determine whether a project is financed by the public or private sector, but they do not define how the project is financed or owned. Financing arrangements typically evolve over the life of a project, from construction through operation. Different funding instruments may be used at each stage, revenue streams are secured through separate contractual or regulatory mechanisms, and economic ownership may differ from legal ownership. This section examines these aspects in turn.

Ownership (Legal Title and Economic Interest)

Ownership can refer either to legal ownership of the asset or to economic ownership of the project. Legal ownership determines who holds title to the asset, while economic ownership relates to who benefits from the project’s cash flows and bears its risks. These two concepts do not always align. As a result, understanding who ultimately controls and benefits from a project requires examining both the ownership structure and the allocation of economic rights.

Financing the Build Phase (EPCF)

During construction, financing may be provided through an Engineering, Procurement, Construction and Financing (EPCF) structure, under which a single contractor is responsible for engineering, procurement, construction and financing. Financing is often supported by export credit agencies (ECAs), allowing projects to access funding alongside delivery of the asset. This approach is particularly common in emerging markets, where it can simplify project execution and facilitate access to capital. However, it also increases reliance on a single counterparty for both construction and financing.

Financing the Operate Phase (OMF)

Once a project becomes operational, financing is generally supported by the asset’s operating cash flows rather than by construction arrangements. As construction risk declines and revenues become more predictable, projects can often be refinanced under more favourable terms. This transition from construction-stage financing to operational financing is a key value-creation milestone, allowing equity investors to realise part of the value generated during development and delivery. This stage is sometimes referred to as Operations, Maintenance and Financing (OMF), reflecting the focus on the long-term operation of the asset and the financing supported by its ongoing cash flows.

Securing Revenue through a PPP

Public-Private Partnerships (PPPs) are procurement frameworks that define how responsibilities, risks and payments are allocated between the public and private sectors. Two main payment mechanisms are commonly used. Under a user-pay model, revenues are generated directly from end users, with the private operator bearing demand risk. Under an availability-payment model, the public authority makes periodic payments subject to performance requirements, while retaining demand risk. The choice of payment mechanism is a key determinant of project risk allocation and bankability.

Securing Revenue through a RAB

The Regulated Asset Base (RAB) model is a financing framework commonly used for monopoly infrastructure assets such as utility networks. Developed in the United Kingdom following the privatisation of water, electricity and gas networks in the late 1980s, it allows operators to recover operating costs, depreciation and a regulated return on invested capital through revenues set by an independent regulator (Slaughter and May, 2025).

By providing stable and predictable cash flows, the model reduces revenue risk and lowers the cost of capital, making it attractive to long-term investors such as pension funds and insurance companies. The Thames Tideway Tunnel project in London is a notable example of the RAB model in practice. Its success ultimately depends on the credibility and stability of the regulatory framework.

Risk Allocation and Bankability

The choice of project structure is primarily driven by risk allocation in project finance structuring. In project finance, risks are allocated to the parties best positioned to manage them. As a result, the structure, financing arrangements and revenue model are designed to distribute risks efficiently between stakeholders.

In practice, construction risk is typically allocated to the contractor through an EPC contract. Demand risk may be borne either by the public sector, through availability payments, or by the private operator under a user-pay model. Operational risk generally remains with the operator, which is responsible for the asset’s performance throughout its life. Political and regulatory risks are managed through regulatory frameworks, government support measures or risk mitigation instruments. Ultimately, a project’s bankability depends on an appropriate allocation of risks among all parties involved.

Talk to our team

If you are considering a project-financed infrastructure opportunity and need support on commercial structuring, lender-ready financial modelling, or bid execution, get in touch with our team at info@gi-advisors.com.

Stay ahead of the curve

Follow us on LinkedIn to receive regular updates on how to successfully develop large-scale infrastructure.

References :

- Highways Agency (2009) £6.2 billion M25 Design, Build, Finance and Operate (DBFO) contract awarded. Press release via WiredGov, 20 May.

- National Infrastructure and Construction Pipeline (2024) Analysis of the National Infrastructure and Construction Pipeline 2023. UK Government.

- Gorton G.B. & Souleles N.S. (2005) Special Purpose Vehicles and Securitization

- Esty B.C., Chavich C. & Sesia A. (2014) An Overview of Project Finance and Infrastructure Finance—2014 Update. Harvard Business School Background Note No. 214-083.

- Energy-Storage.News (2024) Inside South Australia’s 1.3GW FERM tender: Why a technology-neutral process produced an all-battery outcome.

- PV Magazine (2026) Mining company opens 30 MW solar tender in Botswana. Article for PV Magazine, 17 June

- Slaughter and May (2025) Regulated Asset Base Models: Their role in energy and infrastructure investment in the UK.

- Wells, B. A., & Wells, K. L. (2026, March 9). Oklahoma’s King of the Wildcatters. American Oil & Gas Historical Society. https://aoghs.org/petroleum-pioneers/wildcatter-tom-slick/

- Macalister, T. (2014, October 11). The Forties oil field is 50, but there are no happy returns in the North Sea now. The Guardian. https://www.theguardian.com/business/2014/oct/12/forties-oil-field-50-north-sea-uk-offshore-bp

- Parker, H. (2025, June 11). Eurostar trains to Switzerland and Germany are an empty promise. The i Paper. https://inews.co.uk/inews-lifestyle/travel/eurostar-trains-switzerland-germany-empty-promise-3739966