PPP Financial Advisory in Saudi Arabia and Vision 2030

Introduction

Saudi Arabia’s Vision 2030 programme has moved PPPs to a nationwide procurement pipeline across transport, utilities and selected social infrastructure. For sponsors, the differentiator is increasingly not technical capability alone, but the ability to evidence bankability early and convert contract mechanics into lender-ready cashflows.

This article explains what PPP financial advisory in Saudi Arabia (KSA) looks like in practice, and the modelling and structuring issues that most often determine whether a bid is financeable.

Saudi Arabia Infrastructure Context

Since the Kingdom’s unification in 1932, infrastructure has been a core tool for state-building, economic development, and national integration. Saudi Arabia’s modern infrastructure story can be read in three phases:

Early Foundations (1932 – 1970s).

Following the first discovery of commercially viable oil at Dammam Well No.7 on March 4th 1938, infrastructure investment prioritised national connectivity through early road links and foundational rail assets (Rizvi, 2025). The Dammam-Riyadh railway (construction commencing in 1947; inaugurated in 1951) and the later creation of national rail governance (including the establishment of the Saudi Railways Organization in 1966) set early delivery and institutional foundations (SAR, 2026).

The First Boom (1970s-1980s)

The first boom of the 1970s-1980s saw the start of formal national development planning in 1970. This triggered a major oil-funded expansion of public capex, rapidly scaling core networks of roads, ports, utilities, and urban infrastructure at unprecedented pace. By the end of the Third Development Plan in 1985, academic assessments estimate around SAR 375 billion had been allocated to development infrastructure (Looney, 1990).

Vision 2030 Era (2016 – Present)

Under Vision 2030, infrastructure investment increasingly supports diversification (tourism, logistics, advanced industry and the digital economy) and is delivered through scaled sovereign platforms (including PIF) alongside a more formalised PPP / privatisation programme. NCP’s 200-project, 17-sector pipeline signals a shift toward a repeatable PPP market with more predictable deal flow and increasingly standardised, lender-facing approaches for sponsors, lenders and government counterparties. (De la Maza, 2025).

As this pipeline matures, procurement is expected to become more programmatic and bankability-driven. In this context, demonstrating lender-ready bankability early is increasingly central to whether PPPs progress from pipeline to contract

Introduction to PPP financial advisory

PPP financial advisory is the workstream that turns a technical and commercial solution into an executable, financeable bid. It ensures the project’s risk allocation, payment profile and contractual mechanics translate into a bankable cashflow profile that can be financed on competitive terms within the procurement timetable.

In a live PPP bid, the financial advisor typically leads three linked activities:

1. Develop and continuously refine a rigorous bid model reflecting the evolving bid position, local financing terms and tax treatment, and able to withstand lender downside cases.

2. Shape and run the financing strategy, engaging lenders early and securing credible funding appetite (and, where required, commitments) in parallel with the bid process.

3. Produce lender-facing materials and manage lender diligence (teasers, information packs, model governance and Q&A) so the financing proposition remains consistent, defensible and executable through submission and into financial close.

PPP financial advisory is therefore a bankability and execution discipline requiring tight integration of commercial terms, financial modelling and lender engagement within bid and award deadlines.

From preferred bidder to financial close, the focus shifts from positioning the financing to executing it: converting indicative terms into diligenced lender documentation, managing lender Q&A and conditions precedent, supporting negotiations on bankability-critical clauses, and driving the model through final credit approvals to close.

Saudi Arabia-Specific Bankability & Modelling Considerations

Bankability issues in any PPP market are largely mechanical. Lenders will test:

Payment Mechanism

- Clearly defined and enforceable (availability-based vs. user-paid vs. tariff-backed).

Downside Protection

- Termination and compensation outcomes protect senior debt.

Risk Allocation

- PPP agreement, EPC and O&M responsibilities are clean, so delays, performance failures, or third-party dependencies do not leave the project company carrying unpriced “interface” risk.

These tests translate directly into the model through revenue stress cases (including deductions where relevant), construction delay sensitivities, reserve requirements, covenant sizing and distribution lock-up mechanics.

Unique Modelling Challenges Particular to Saudi Arabian Projects

In KSA, bankability also turns on tax and cross-border frictions because they change the tax block, cashflow waterfall and ultimately debt sizing. In mixed-ownership structures, corporate income tax (CIT) and Zakat can both apply broadly in proportion to shareholder type, CIT commonly applying to the non-Saudi/GCC share of taxable profits and Zakat applying to the Saudi/GCC share (GrantThornton, 2025). This drives how the model allocates post-tax cashflows and forecasts distributions.

Zakat is assessed on a defined “Zakat base”. The Zakat base is a balance-sheet-anchored modified net worth, not simply profit or EBT. A credible model therefore often needs a dedicated Zakat-base schedule rather than a single tax line. Because the base is built from balance sheet components with specific additions and deductions, modelling can create circularities (e.g., cash/reserve movements and retained earnings affecting the base that drives the Zakat charge), requiring clear base definitions, period-end conventions and iteration controls where required (ZATCA, 2025).

Lender diligence in KSA routinely tests cross-border payment leakages, particularly where services or other payments to non-residents trigger withholding tax (WHT) and corresponding gross-up / recoverability assumptions (ZATCA, 2021). The practical implication is that KSA bankability often requires:

- (i) an ownership-apportioned tax design,

- (ii) a balance-sheet-driven Zakat computation that lenders can follow, and

- (iii) explicit treatment of WHT frictions in the cashflow waterfall and sensitivities.

Financing Landscape for PPPs in KSA

KSA’s PPP financing market is built around repeatable project-finance structures in contracted infrastructure and is scaling alongside the government’s PPP pipeline. NCP’s have a published pipeline of 200 privatisation and PPP opportunities. This signals sustained procurement volume and continued financing demand across sectors.

Senior debt is typically anchored by Saudi and regional banks, which have expanded project lending in line with Vision 2030 activity (Saeed, 2026). International lenders participate more selectively, mainly from established European and Asian project-finance institutions:

Europe

- Standard Chartered, HSBC, Crédit Agricole CIB, Société Générale and KfW IPEX-Bank are often cited among the more active international lenders in the Kingdom (PFI, 2024).

Asia (Japan)

- PIF has announced MoUs worth up to USD 51bn with major Japanese financial institutions including MUFG, Mizuho, SMFG, JBIC and NEXI (PIF, 2024).

This supports the Vision 2030 agenda to expand private participation and leverage private capital and expertise in the delivery of public infrastructure and services.

Saudi Arabia PPP Case Studies

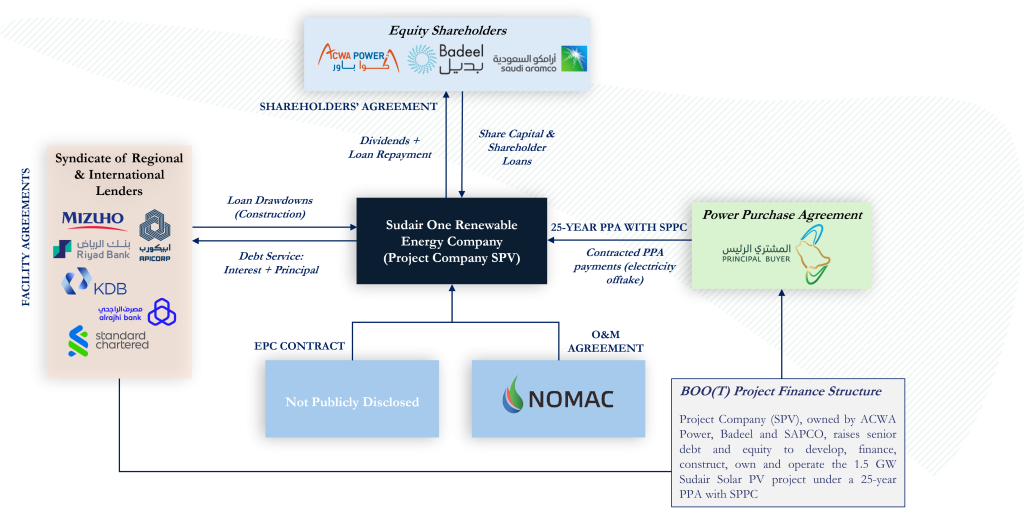

1. Sudair Solar PV IPP – 25 year Power Purchase Agreement PPA with the Saudi Power Procurement Company

Deal Pros

- 25-year PPA with SPPC anchors contracted revenues and removes merchant demand risk

- Mini-perm debt shifts lender focus to refi/linancing risk, so sizing is driven by conservative cashflows and strong covenant headroom

Deal Cons

- Multi-bank syndication means multiple credit committees must underwrite the same story, so inconsistent assumptions between model, PPA mechanics and technical basis become a bankability risk (Bellini, 2021)

High-level project company structure

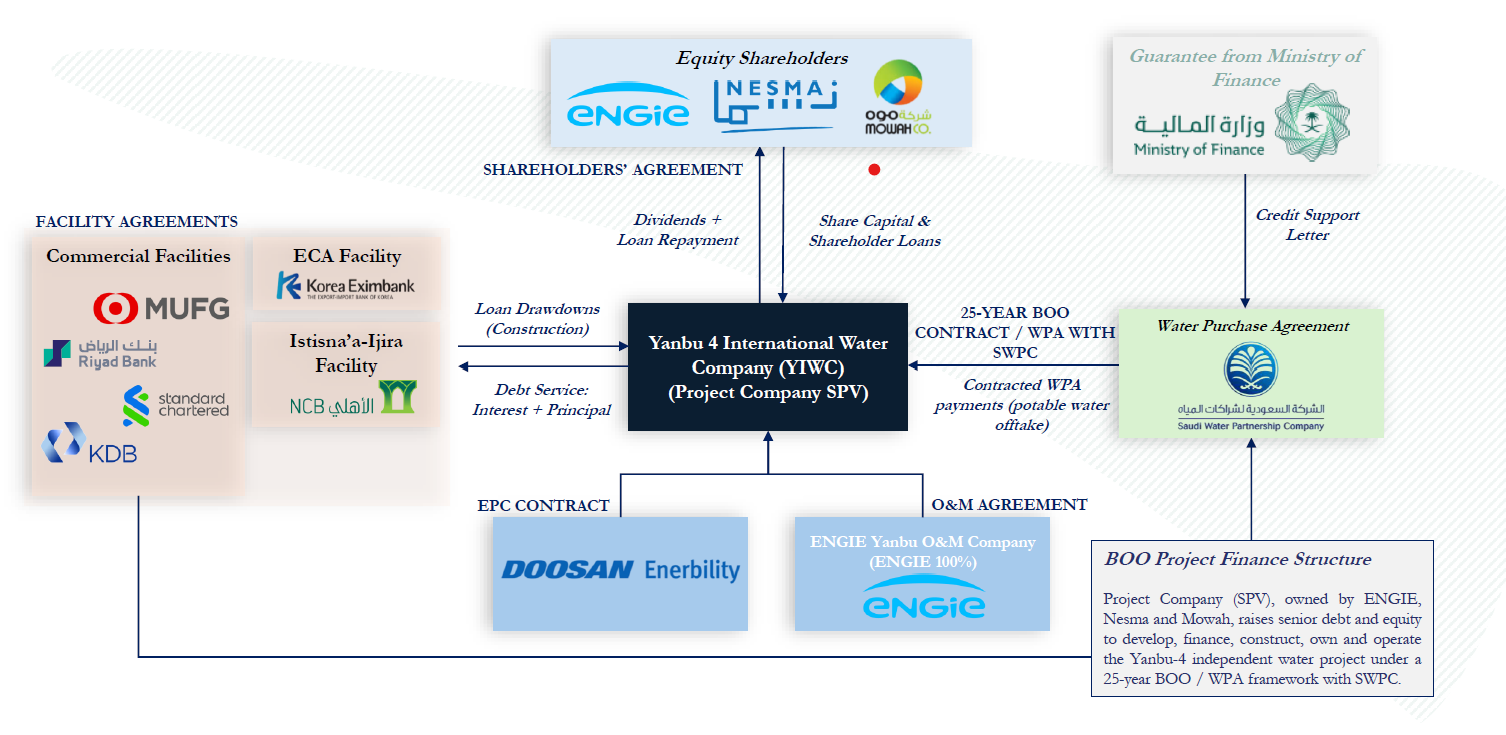

2. Yanbu 4 Reverse Osmosis Desalination IWP – Long-term Water Purchase Agreement (WPA) with Saudi Water Partnership Company

Deal Pros

- MoF credit support underpins SWPC WPA payments, adding further security to 25-Year WPA and strengthening lender comfort (DLA Piper, 2021).

Deal Cons

- Mixed facility package: commercial tranche plus NCB Istisna’a-Ijara and KEXIM facility, so execution hinges on clean lender coordination

- Bundled plant + transmission scope concentrates schedule/interface risk, so the model needs tight completion and delay logic

High-level project company structure

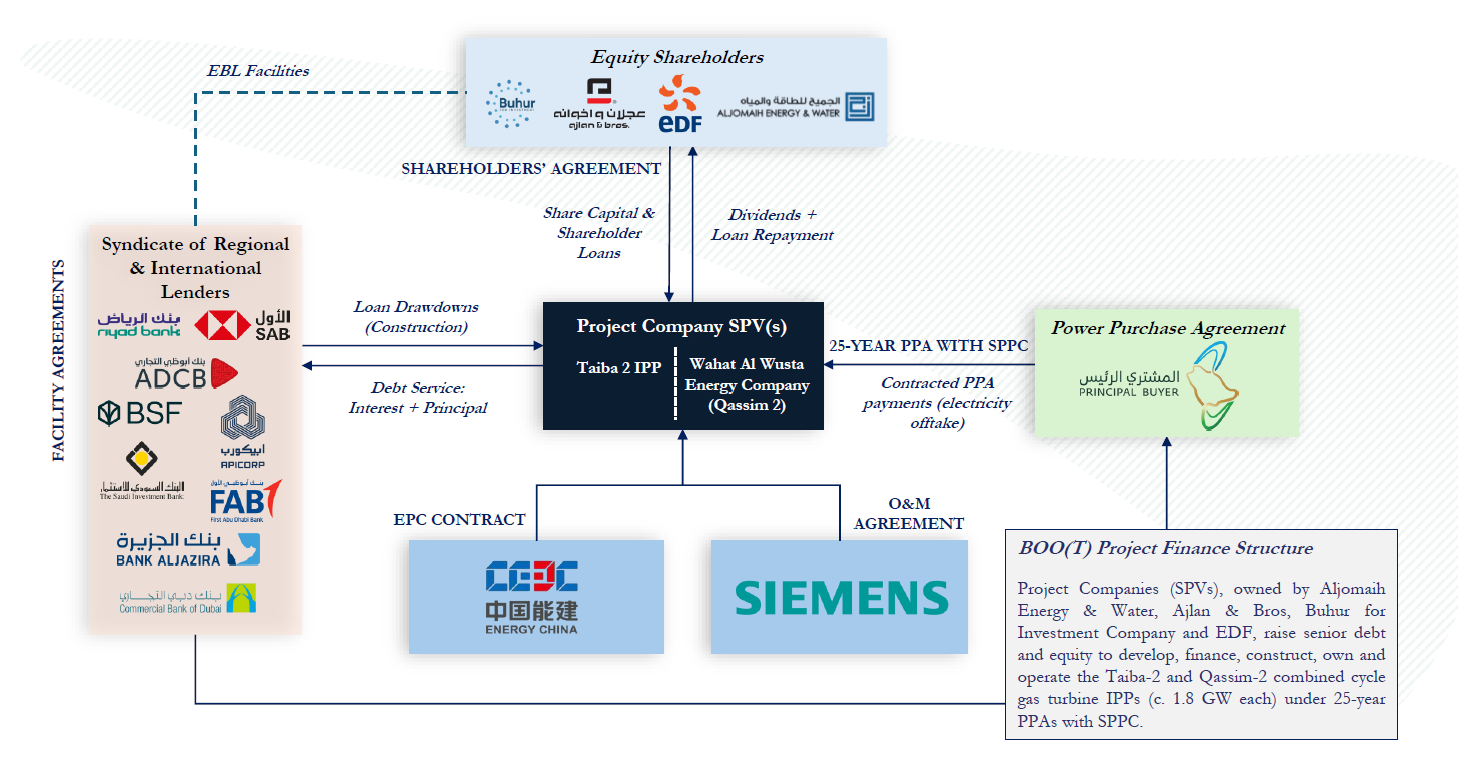

3. Taiba 2 & Qassim 2 Combined Cycle Gas Turbine IPP – 25 year Power Purchase Agreement PPA with the Saudi Power Procurement Company

Deal Pros

- First KSA IPPs with a carbon-capture provision, supporting long-term compliance optionality.

- OEM-backed delivery with a 25-year Siemens Energy maintenance contract, strengthening availability assumptions.

Deal Cons

- Large capex and debt quantum (c. USD 3.9bn) increases refinancing and execution sensitivity.

- Two-stage commissioning with simple-cycle in 2026, and combined-cycle later, adds testing and interface risk.

Conclusion

As KSA’s PPP market matures, financing is becoming more standardised but not simpler. Lenders still underwrite the mechanics, and transaction execution still depends on translating contract terms into lender-ready cashflows at pace to meet award timetables.

With deal volumes rising and a repeatable pipeline across utilities, transport and selected social infrastructure, small modelling and diligence details increasingly drive outcomes. Ownership-apportioned CIT and Zakat (including the balance-sheet-driven Zakat base) can materially shift post-tax cashflows, and withholding tax leakage on cross-border payments can erode value if not structured and modelled explicitly. In practice, “bankability” is evidenced through lender-ready modelling and early lender engagement that make these mechanics transparent, financeable and executable within the procurement timetable.

Talk to our team

If you’re considering a PPP or project-financed infrastructure opportunity in Saudi Arabia or other global markets and need support on commercial structuring, lender-ready financial modelling, or bid execution, get in touch with our team at info@gi-advisors.com.

Stay ahead of the curve

Follow us on LinkedIn to receive regular updates on how to successfully develop large-scale infrastructure.

References

- Rizvi Rahman F. (2025) The desert pioneer behind our first oil discovery. Article for Aramco, 10 December.

- Saudi Arabia Railways [SAR] (2026) Our Story.

- Looney R.E. (1990) Infrastructure Investment and Inflation in Saudi Arabia. Journal of Energy and Development, vol 14, no.1, 1990.

- De la Maza (2025) Public-Private Partnerships in Saudi Arabia: Trends, Frameworks, and Investment Opportunities. Article for Aninver, 22 March.

- GrantThornton (2025) Zakat vs. Corporate Tax: How Multinationals Can Navigate Dual Obligations.

- Zakat, Tax and Customs Authority [ZATCA] (2025) Zakat General: Simplified Guideline.

- Zakat, Tax and Customs Authority [ZATCA] (2021) Compiled Resolutions and Circulars Regarding Withholding Tax: Pursuant to the Income Tax Law & its Implementing Regulations.

- Saeed N. (2026) Saudi banks drive Arab project lending activity. Article for Zawya, 27 January.

- Public Investment Fund [PIF] (2024) PIF Signs memorandums of understanding with five leading Japanese financial institutions. Press release, 31 October.

- PFI (2024) Middle East & Africa Awards

- Bellini E. (2021) Financial Close for 1.5 GW Solar PV Project in Saudi Arabia. Article for pv magazine.

- DLA Piper (2021) Yanbu 4 IWP and its transmission pipe.

- National Geo [NG] (2014) https://www.nationalgeographic.org/society/

- Elsheshtawy Y. (2019) A Flâneur in Riyadh: The Transformation of Tahlia Street

- Shirazibustan (2023) File:Riyadh, Saudi Arabia. Palaces in al-Futa, in 1970.jpg

- Buekenhout N. (2024) Latest Updates on Saudi Arabia’s Top 13 Mega and Giga Projects Article for MEPMiddleEast

- NS Energy (2021) Sudair Solar Power Plant

- MUFG (2021) MUFG closes financing of Yanbu 4 IWP in Saudi Arabia

- Reuters (2021) Saudi Electricity raises nearly $2.6 bln with revolving loan

- Linklaters (2024) Linklaters advises SPPC on landmark procurement and financial close of four greenfield IPPs in Saudi Arabia

- EDF (2024) Taiba 2 & Qassim 2 Combined Cycle Gas Turbine (CCGT)

- Siemens (2024) 1.5 billion US-Dollar order for Siemens Energy in Saudi Arabia: Efficient combined cycle power plants for the country’s energy supply

{kind=link}